Week ended May 8, 2026: market remains constructive

- tim@emorningcoffee.com

- May 9

- 6 min read

I started penning this update with my recurring rant about the antics of the Trump Administration. The daily “war is over” rhetoric coming from the leader of the free world is super-annoying, especially since Iran and the U.S. remain more or less deadlocked, with the Strait of Hormuz closed and no oil flowing through it. But does this really matter anymore, at least to investors?

Yes, higher oil prices are hurting consumers (see “Consumer confidence” below) and will reverberate through the broader global economy, but stock investors don’t really seem to care one iota. Investors have pivoted their focus back to A.I. productivity improvements in the quarters and years ahead, relegating geopolitical tensions to the rubbish bin as corporate earnings continue to march higher. I was reasonably confident that higher oil prices would dampen enthusiasm for stocks, but I have most certainly been proven wrong, at least in the U.S. which remains far removed from the conflict zone. Moreover, the U.S. is the epicentre of all-important A.I. The war has certainly splattered Europe though, with U.K. and broader European stocks reclaiming their place as global laggards after a run in 2025 that saw European stock markets outperform U.S. stocks. Ah….the world order has returned to normal, at least for the time being!

Dire scenarios can easily be cooked up about U.S. stocks and bonds as we look forward. However, downplaying the size, diversity and momentum of the U.S. economy is unwise if you want to generate attractive investment returns. There’s no use moaning about the Trump Administration, at least if you’re an investor, because what he does and says largely seems to matter little at this point. Investors are onto his strategy of “throwing shit on the wall and seeing what sticks”, and his capitulation time and time again (TACO) is well documented and understood by astute investors. So the best advice I can offer investors is simple – don’t sit this rally out, because there have been more ups and downs than can be imagined since Mr Trump took office. And so far, during every dip, investors eventually come around to saying “so what”, and they pile back in with a vengeance.

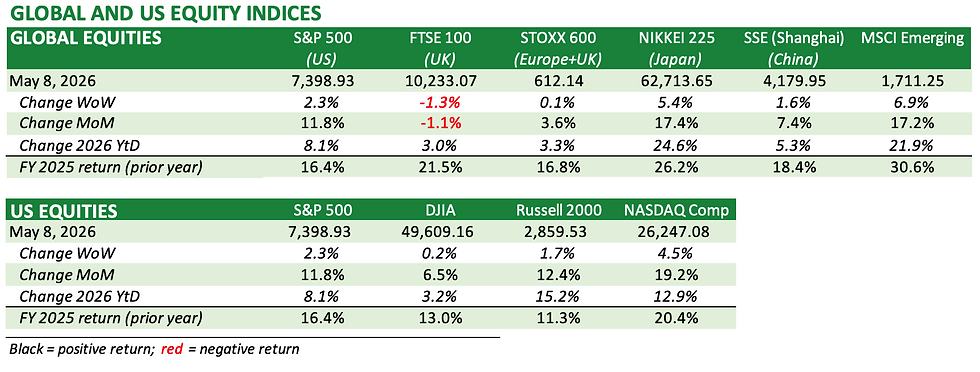

Markets last week

European stocks continue to lag Asian and U.S. stocks, with the best performers this past week being the Nikkei 225 (Japan) and emerging markets stocks (MSCI EM index). The FTSE 100 lost ground and is - relatively speaking - the worst performing equity market tracked by EMC YtD, with the STOXX 600 (broader Europe) not far behind.

U.S. stocks were better across the board, with the S&P 500 increasing for the sixth consecutive week. Both the S&P 500 and the NASDAQ closed the week at record highs (again). Tech shares led the advance, with the NASDAQ gaining 4.5% on the week, adding to its 12.9% gain YtD.

U.S. Treasury bonds were little changed on the week, although Friday’s job report strengthened the case for no Fed Funds rate reductions this year. Yields at the short end of the curve were a touch higher. Corporate bonds were largely steady in both investment grade and high yield, although European high yield bonds had a solid week as far as performance.

Oil prices fell sharply early in the week, and then stabilised. The price of oil remains severely elevated and continues to oscillate based on the latest claim – or not – that a long-term solution to the situation between Iran and the U.S. is “just around the corner.” The U.S.-Iran stalemate seems static, certainly far from resolved as the Gulf of Hormuz remains closed. A stalemate looks to be well-received by aggressive buyers of risk, as silly as that might sound.

The greenback and Yen were little changed on the week, and gold and Bitcoin were both slightly better bid.

The table below summarises performance last week, with more detailed tables contained in the "Markets" section at the end of this update.

What mattered last week

U.S. jobs report

As a case in point as to the resilience of the mighty U.S. economy, more than twice the number of new jobs were added in April than were expected by analysts, according to the jobs report released Friday. The unemployment rate remained steady at 4.3%, suggesting that caution around the war with Iran is more or less “meh”, at least on the surface. The strong U.S. jobs market is great news for investors, although it is less good news for investors hoping for lower interest rates. In fact, the CME FedWatch Tool is now attaching some probability to the Fed increasing interest rates starting in the autumn. Can you imagine what Mr Trump would have to say? Yields reacted by largely remaining steady on Friday, reflecting the expectation that the U.S. economy remains largely biased towards a combination of decent growth and persistent above-target inflation.

Consumer confidence

Consumer confidence was an entirely different matter, as Friday’s release of the University of Michigan Consumer Surveyindicated. The UofM Index of Consumer Sentiment came in at 48.2, the lowest level since the survey started in 1952. This reflects the reality of the U.S. K-shaped economy, with the top 1% (or perhaps slightly more) of people “partying like it’s 1999” while the rest of the country suffers from uncertainty associated with higher prices at the pump and the unpopularity of the Iran-U.S. war. Perhaps the silver lining in the survey was that inflation expectations moderated somewhat.

Other news

In other news, Berkshire had its first “Woodstock-like” annual shareholders meeting not chaired by Mr Buffet, although he remains a Director of the company and was seated in the first row. New Berkshire head Greg Abel chaired the annual investor forum, before which the company’s 1Q26 earnings were released (press release here, 1Q26 10-Q here). Sticking with the Buffet-Munger theme of ultimate conservatism, CEO Abel – like Messrs. Buffet and Munger before him – seems in no rush to deploy the company’s growing cash hoard of nearly $390 billion. I have tried to put this huge amount in context. $390 billion of cash would mean that – ignoring all other businesses of Berkshire and just valuing it at cash – the company would be the 23rd largest company by market cap in the S&P 500, just ahead of Bank of America and just behind Caterpillar. From a country GDP perspective, Berkshire’s cash hoard ranks just below Pakistan, which is the 45thlargest country in the world by GDP (2026 est, per IMF). With all this cash and little to do with it, investors needs to remember that the company is always supporting its own stock through buybacks, since it does not pay a dividend. (For disclosure, Berkshire for now remains the largest holding in my portfolio.)

OPEC+ announced early last week that it was raising its output in June for the third consecutive month, although this seems largely symbolic (and irrelevant) given the disruption to oil supplies occurring because of the ongoing blockage by Iran of shipments through the Strait of Hormuz. Also, the UAE announced that it was leaving OPEC. It begs the question – with the cartel fraying and the U.S. being energy independent, how long with this cartel last? And does it really matter anymore?

What I’m doing portfolio wise

I lost some shares of AMZN and GOOG (via covered calls) into earnings week before last, although I was not disappointed at the levels given the recent run of both stocks. However, tech generally – including these two excellent stocks – have headed even higher since. I had my usual predictable reaction – I wrote another series of covered calls this past week on AAPL (the runner now), GOOG and AMZN. With tech stocks gapping higher day after day, they are commanding a higher percentage of my portfolio even as I lighten in select names, ceteris paribus.

Away from the hyperscalers, I find myself again scratching my head at CRWD with the price above $500/share. Recall that I sold nearly my entire position in mid-2025, and then reloaded at the end of February when the shares were in the mid $300’s area. I would like to have cybersecurity exposure, because I think cyberattacks / disruptions are a rapidly growing risk as we move forward. However, CRWD suddenly gapped up, increasing 36% in the last month alone. With a forward P/E of 98x and a price-to-sales of 24.8x, I have to take my money off the table, and again – for now – say “adios” to CRWD. I might be proven wrong, but my instinct is that I will get another bite at that apple.

Aside from these minor portfolio adjustments, I am just riding it out. Gains day after day are seductive. In fact, being long stocks / stock indices requires limited intellect. It’s just a matter of being “in it to win it”, ensuring you have portfolio diversification (asset class, geography, sector, etc) that is in line with your personal risk profile, and maintaining the unwavering conviction to stay the course during increasingly severe market gyrations.

MARKET DATA AND TABLES

Below are tables of key indices and asset prices that have been updated for the past week.

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments