Week ended May 15, 2026: In bonds there is truth

- tim@emorningcoffee.com

- May 16

- 7 min read

Robust demand for anything A.I.-related pushed tech shares in the US and Asia (mostly Korea and Taiwan) higher in the first part of last week, continuing a trend that has propelled U.S. stocks to double digit returns since the beginning of April. As I wrote last week, earnings have generally been supportive of stocks, and the U.S. has benefited from being far removed from the conflict zone in a war it initiated. However, you know my mantra by now – in bonds there is truth.

Last week was not a good week to be a bond investor anywhere in the world, as yields marched higher in nearly all developed markets, led by U.S. Treasuries. The culprit was hotter-than-expected retail and wholesale inflation reports for April, released mid-week, and the ongoing stalemate in the U.S.-Iran war. The Strait of Hormuz remains closed, and in spite of all sorts of blatant innuendo to the contrary, it seems from my vantage point that Iran holds enough of the cards to drag out this situation as long as they want. This is keeping oil prices elevated and volatile, with the price reacting to the latest news. This, in turn, is adding inflationary pressures that have now become visible in the latest data. And more concerning, higher oil prices for much longer than expected are feeding into higher inflationary expectations, which in turn are feeding into the bond market. And herein lies the problem.

Sooner or later U.S. stocks had to crack, and crack they did on Friday giving back all of their weekly gains and more. Dip buyers will probably step in as we have become accustomed to, but it is higher yields I fear the most, because:

Higher yields raise the discount rate for valuing stocks (resulting in lower present values),

Higher yields mean that companies will have to pay more for borrowing money, degrading their creditworthiness, and

Higher bond yields cascade into the residential mortgage and other consumer lending markets, worsening the position of the almighty U.S. consumer, the growth engine of the world’s largest and most robust economy.

Keep in mind that higher yields are the effect not the cause though. The cause of higher bond yields is higher inflation expectations, and higher inflation kicks consumers squarely in the knees from the perspective of affordability.

The winners more or less since the pandemic have been people fortunate enough to be long stocks. In the long run, stocks always go up. However, I increasingly struggle to digest the reality that “stocks always go up” when every week and every month is higher than the last. Wealthy folks – or simply those with positive net worth to perhaps be more accurate – have benefited enormously from the wealth effect of increasing asset prices. As I have said many times, you really don’t have to be that smart – you just have to be long stocks to have benefited. But imagine if the gloss came off of equities in a bigger way? The negative wealth effect would be similar to deflation in that once it becomes the new norm, it would become entrenched and would be very difficult to unwind.

I don’t really want to think about this more, because Friday was just one day – an off day perhaps – in a financial context in which things right themselves quickly and return to their upward trajectory on a dime. Equities are a bit of a children’s game though compared to the “adults in the room” bond market, and we – as investors – need to cross our fingers and hope that we are seeing a one day blip in yields and nothing more sinister.

Markets last week

Global equities were mixed this past week, with a strong fade occurring on Friday. European bourses continue to feel the brunt of effects of higher oil prices, and the U.K. is manufacturing its own political crisis that is weighing on U.K. stocks and bonds (and Sterling). Asian equities also experienced a tech fade towards the end of the week, pushing stocks lower in the region.

U.S. stocks nearly held onto their weekly gains in spite of Friday’s selloff, although the session to end the week was ugly and most of the week’s gains were surrendered. Although the run has been hard and fast since early April, and economic warning signs largely been ignored to date, it seems that yields spiking on Friday finally caught the attention of even the most sturdy U.S. stock investors.

As mentioned already, bonds were certainly not the place to be last week, with higher-than-expected CPI and PPI data in the U.S. confirming what lies ahead as far as oil-induced higher inflation. Treasury auctions went poorly (discussed further below), as yield across the belly and long end of the curve approached levels not seen for some time. Corporate bonds followed suit, heading lower too because of higher underlying yields even as spreads were largely stable, at least through Thursday (last data point for corporate bonds).

The Dollar largely held its grown as the US -Iran situation drags on. Oil was higher on the week, and gold lower.

See "Market Tables" section below for more detail.

WHAT MATTERED LAST WEEK

UK politics

If you live in the U.K. you are certainly aware of the political turmoil (again) affecting the U.K. With the government on its fifth prime minister since 2016 (post BREXIT, post David Cameron), the new Labour government appears to be in shambles with current PM Kier Starmer hanging on by his fingernails. I suspect he is a goner as his party supporters slowly abandon him one by one, although the question as to who would replace him seems far from clear. One thing is for certain – there will be no snap election because Labour would get trounced. And I doubt the Conservatives would do much better. This would leave a dog’s breakfast of (traditionally) secondary parties vying to run the country. Although Reform certainly seems to be the most viable at this point, I struggle to imagine the iterations of a winning non-majority party trying to form a coalition – yikes!! But fear not – Labour would not be silly enough to call for an election it would most certainly lose, so here we sit until 2029. Putting that hypothetical aside, the current inter-Labour turmoil is rocking markets and is severely testing the nerves of investors. U.K. Gilts (government bonds) and Sterling are under severe pressure, with the yield on the 30-year Gilt reaching its highest level last week since 1998. To be fair, the war between the U.S. and Iran has also contributed to uncertainty with inflation re-surging, but much of this crisis feels to be like a Labour own goal.

30-year US Treasury auction: yield above 5% for first time since 2007

The U.S. Treasury auctioned its highest coupon 30-year debt since 2007 mid-week, following the “hot” CPI and even hotter PPI reports for April released earlier in the week. In order to entice investors, the Treasury had to hang a coupon north of 5% (5.046%) on the 30-year bonds to attract enough interest to complete the auction of $25 billion of Treasuries. And yields continued to inch higher the rest of the week, not a good look for the U.S. although nearly every other global bond market also felt the pressure as inflationary expectations remain elevated.

US inflation above expectations for April

April’s CPI data, released Tuesday, was slightly worse than expected, with headline inflation now running at 3.8%/annum (due mainly to higher energy costs), and core inflation (ignores energy and food) running at 2.8%/annum. You can read April’s CPI report from the BLS here. Perhaps more concerning was the red hot PPI report for April released on Wednesday (here). PPI (measure of wholesale goods and services prices, and typically a leading indicator for CPI) for final goods increased 1.4% in April (vs March), and 6.0% YoY, the largest increase since December 2022. Similar to CPI, the major culprit was energy prices, although keep in mind that tariffs also have played a role. For both CPI and PPI, the reads were above consensus, and are concerning in that both are broader based than expected.

There are two other things worth mentioning.

Firstly and perhaps most importantly, both headline and core inflation remain well above the Fed’s target of 2%/annum. Concerns about elevated inflation mean that the Fed will have no choice but to adopt a more hawkish stance for the foreseeable future. In fact, the CME FedWatch Tool is now projecting that there is more than a 30% chance that the Fed will increase the Federal Funds rate by the end of this year.

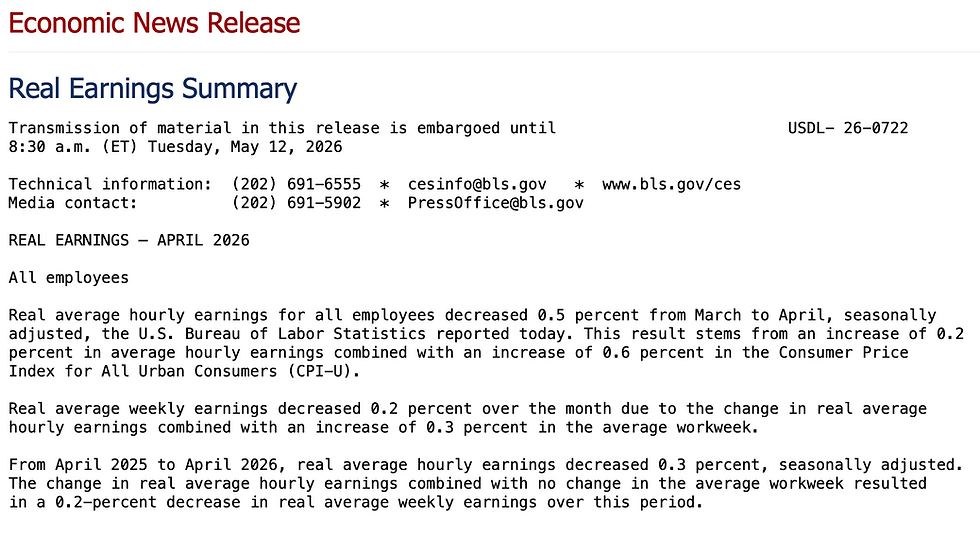

Secondly, whereas wage growth had been exceeding above-target inflation for many months, wage growth has now slowed down sufficiently such that inflation is higher than wage growth. In other words, real wage growth is now negative, and this is feeding into the affordability crisis in America that is becoming more pronounced and real. I think you will find the extract from the BLS “Real Earnings Summary” released on Tuesday interesting:

Alphabet (Google) surges

I had a friend that said to me around 18 months ago that GOOG would die a slow death because A.I. searches would undo the company’s cash cow, its infamous search engine. I didn’t buy that argument one bit for two major reasons. Firstly, GOOG has other revenue streams than search, including a growing cloud business and a leading social media platform in YouTube. And secondly, under no circumstances did I believe that GOOG would simply sit there and have its lunch eaten by “up and coming” A.I. competitors. 18 months ago, GOOG was the cheapest of the Mag 7 stocks, so the valuation was reflecting a dire outcome from A.I. However the market cap of GOOG is approaching $5 trillion ($4.84 trillion, Friday close), as it closes in on the world’s most valuable company, NVDA ($5.23 trillion, Friday close). See the graph below from Bloomberg, and congrats GOOG and NVDA holders!

Also interesting to now is how GOOG is increasingly tapping the debt markets, not just in the U.S., but globally as it has raised around $60 billion equivalent of debt abroad (see #Bloomberg article here).

What I’m doing portfolio wise

As far as my portfolio, I have lightened slightly on tech (AMZN, GOOG, AAPL) the past couple of weeks, mainly by losing shares into covered calls. I really don’t mind at these levels, as I feel I will have opportunities to add these scraps back if things sell off….and I think they eventually will. The one stock about which I feel some remorse is CRWD, which I was thrilled to sell at effectively around $510/share. And then in a matter of days, the stock touched $590/share on Friday. That does not look like good timing at the moment, but my attitude is “win some, lose some”, and I made a good chunk of change even so. Time will tell, but I don’t mind a touch more liquidity at the moment.

MARKET DATA AND TABLES

Below are tables of key indices and asset prices that have been updated for the past week.

_________________

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments