Week ended April 17, 2026: Back to the races!

- tim@emorningcoffee.com

- Apr 17

- 6 min read

I’m starting to ask myself: are stock investors seeing something that the rest of the world is not? How can equities continue to increase day after day – now reaching record levels in the US – given the context of what is certain to be slower global economic growth and elevated inflation ahead? As much as the U.S. President insists that the war is over and sorted, it clearly is not. Having said that, risk markets – which have run like mad the last couple of weeks – were given another shot of adrenaline on Friday when Iran agreed to reopen the Strait of Hormuz, following a cease fire agreement the day before between Israel and Hizbollah.

For an investor like me that is up to his eyeballs in stocks, I am enjoying the surprisingly fast recovery following the economic damage that has been done by the war with Iran. Adding fuel to the risk-on fire, the first series of earnings releases from S&P 500 companies last week was relatively decent (NFLX aside), suggesting that earnings have remained resilient through the first quarter of 2026 (including war-effected March). Even caution from the big US banks on the outlook failed to temper stock investors’ enthusiasm. Anything that even slightly differs from the Trump Administration narrative (meaning “the war is over”, “we bombed them into submission”, “there has been regime change”, etc) gets labelled “fake news” even though it is impossible to discern the truth. Looking at still-elevated oil prices and the bond market, it is pretty clear that the Trump narrative probably is not the reality. As my readers know, I trust the bond market much more than the stock market these days, and the bond market is struggling to keep its head above water in spite of the “feel good” spirits in the stock market. What the hell is going on?

I have to be honest – I really can’t explain it aside from animals spirits. Forward economic fundamentals are clearly worse off than they were before the war started. Investors jumping back into stocks with both feet given the backdrop do not appear to be particularly concerned about the economic damage this war has caused. Perhaps that’s a good thing – live for the moment! But this certainly is not my mantra, and I have become increasingly uncomfortable with this snapback. It feels at times that the world has simply gone bonkers. I suppose one must give street cred to the buy-the-dippers willing to ignore the economic pain that higher oil prices and disrupted supply chains will bring. For investors that have been watching this snapback from the sidelines, they are slowly re-engaging based on FOMO.

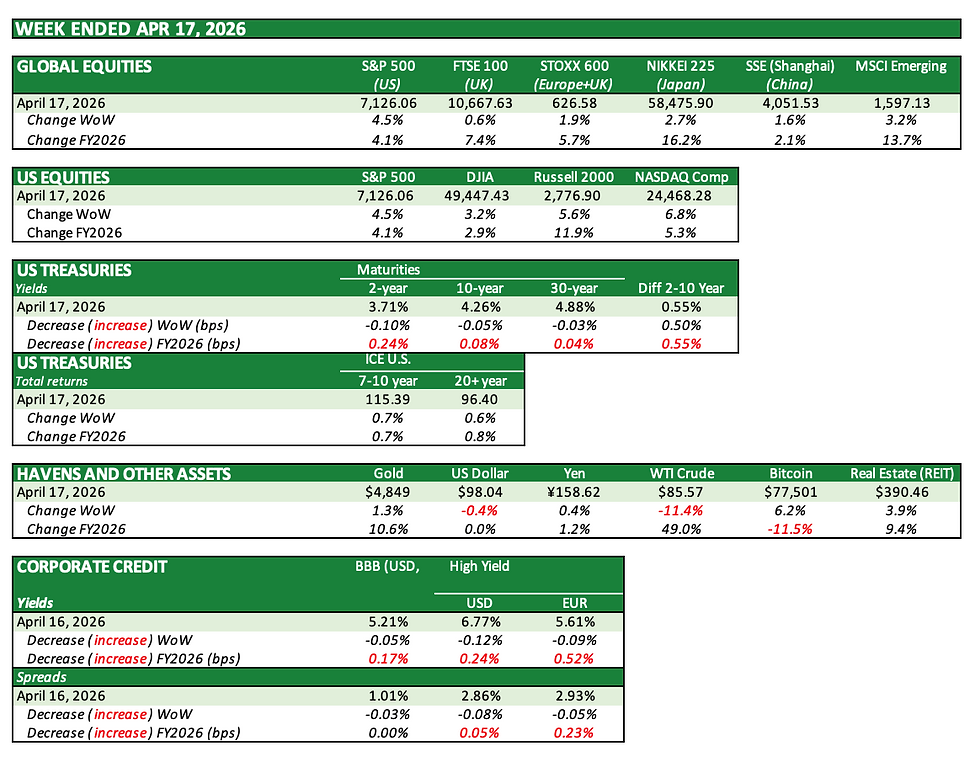

Global stocks continued their recovery across nearly all markets last week, led by emerging markets stocks and U.S. stocks. European stock markets were slightly more tempered, but still powered forward as risk appetite returned. Friday’s party-time sentiment ratcheted up another notch when the announcement came on Friday that the Strait of Hormuz was reopen for traffic. Bond investors remain more nuanced, although bonds also got a boost from Friday’s news with yields falling around 3bps-10bps across the curve WoW, although intermediate and long-term yields are still stubbornly high. The price of crude oil plummeted, and the greenback weakened, both as a result of an improved outlook regarding the end of the conflict. Corporate bond spreads tightened, and both gold and Bitcoin moved higher. The table below illustrates last week’s and YtD performance of the indices and asset prices tracked by EMC.

More detailed tables are at the bottom of this article.

Policy rate increases now look less likely outside the U.S.

I was relieved to read this past week that it now appears both the European Central Bank and the Bank of England have said that it is unlikely that their policy interest rates will be increased in the Eurozone and the U.K., respectively. Yes, inflation has most certainly ticked up, but the damage to economic growth caused by higher energy prices is much more severe than in the U.S. And central bank officials seem to believe that the worst of oil price increases is behind them. As I wrote last week, both the ECB and the BoE are single mandate banks (inflation control only), but they are indicating now that their view is that inflation increases will only be temporary, and the more lasting damage will be slower economic growth in their economies. I think they are right. In any event, I am hoping that they put any thoughts of rate rises on ice for now for the sake of economic growth.

IMF Spring meetings

The IMF spring meetings currently being held in Washington DC will be winding down today, following sessions that started on April 9th. The link above provides information regarding the numerous topical and interesting sessions that have occurred during the last 1.5 weeks. The meeting has featured high-level IMF/World Bank officials, global finance and central bank officials, academics, and other prominent speakers from the public and private sectors. Here is a summary of the five major points from the meeting so far (generated from Google A.I.):

Downgraded Growth & High Uncertainty: The IMF downgraded global growth to 3.1% in 2026, citing persistent conflicts, geopolitics, and trade disruptions as primary drivers of economic instability.

Persistent Inflation & Structural Energy Costs: Elevated energy and fertilizer prices are now deemed structural rather than transitory, creating long-term inflationary pressures driven by conflict-related supply shocks.

Mounting Debt and Fiscal Squeeze: Low-income countries face severe debt distress, with some spending nearly one-fifth of their revenue on interest payments, highlighting an urgent need for global financing solutions.

Geoeconomic Fragmentation: Rising geopolitical tensions are leading to fragmented trade patterns and a shift away from multilateralism, which continues to challenge global financial stability.

Focus on Conflict Costs: Analysis shows that conflict-affected economies experience lasting output losses of roughly 7% within five years, prompting the IMF to integrate conflict risks into long-term macroeconomic surveillance.

And yet the stock market has risen to record levels…..

Trump goes after the Fed again (but now no one takes it seriously)

President Trump is again bringing into question the Fed’s independence, refusing to climb down from what appears to be a frivolous investigation into the Fed’s new HQ’s and the role of Fed Chair Powell, saying this week in the #FT (article free here):

This is as poor as it can get from an acting president, both because it is a threat against the Fed’s independence and is also clearly retribution against the highly respected head of the Federal Reserve for simply doing his job. Moreover, it is another case of Mr Trump suggesting he has powers that he

does not. I wonder at times if the president is the only serious person in government that really thinks the Fed Funds rate should be lower? This sort of tampering even makes the Republican stooges in Congress squirm a bit, although with a few brave exceptions, they simply stand back and let the president speak for the entire party no matter how little sense it makes. If you can’t tell, threatening the Fed’s independence sits very poorly with me, and Mr Trump’s unwillingness to ask his DoJ to climb down will almost certainly delay the Senate confirmation of new Fed head Kevin Warsh. And then what?

What’s ahead?

Central bank meetings:

Bank of Japan: April 27-28 (unclear, but perhaps slight bias towards increase)

FOMC (Fed): April 28-29 (expected hold)

ECB: April 29-30 (expected hold)

Bank of England: April 30 (expected hold)

Earnings of interest, week of April 20: GE, UAL, BA, T, TSLA (Weds pm), IBM, INTC, PG. Note that MSFT, AAPL, AMZN, GOOG and META are all week of April 27th.

Economic data worth watching:

US: retail sales and preliminary April PMI data (manufacturing and services), retail sales (March), consumer confidence survey

UK: employment data, preliminary PMI data (manufacturing and services), retail services, CPI (March)

Eurozone: preliminary PMI data (manufacturing and services)

Japan: CPI

MARKET DATA AND TABLES

Below are tables of key indices and asset prices that have been updated for the past week.

_________________

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments