Week ended April 24, 2026: stocks add to gains in spite of outlook

- tim@emorningcoffee.com

- Apr 25

- 5 min read

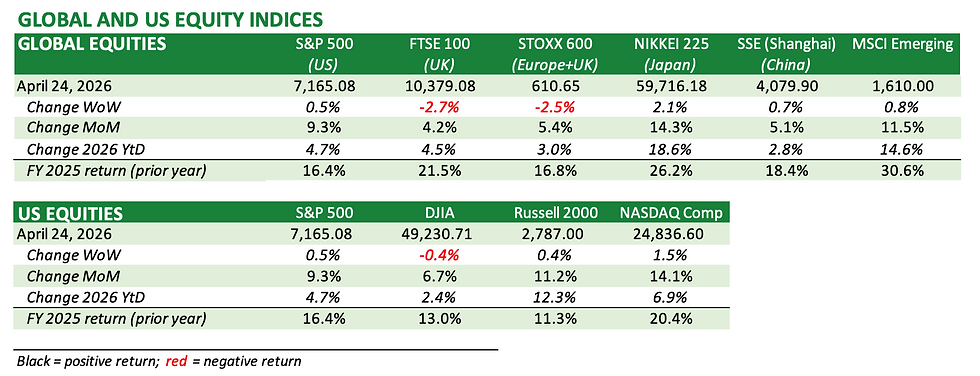

U.S., Asian and emerging markets stocks led gains this past week, while European stocks floundered. Both the S&P 500 and the NASDAQ closed the week at record highs, driven by sizzling tech share performance from the likes of INTC (+20.5% WoW, earnings beat and raised guidance), AMZN (+5.4% WoW, series of positive events, record high), ARM (+40.8% WoW), AMD (+24.9% WoW) and NVDA (+.3.3% WoW, passed $5 trillion market cap). Even as U.S. stocks continued their ascent, US Treasuries and USD-denominated corporate bonds lost ground as yields headed higher. Oil prices increased double-digits again as a peace agreement in the U.S.-Iran conflict remains elusive. The greenback strengthened due to higher geopolitical uncertainty, with gold selling off and Bitcoin holding on to recent gains. The table below is an update of weekly and YtD performance of select indices and asset classes, with more detail available in the market section below.

I wrote in mid-March that markets would bottom out once the Middle East situation was resolved or the conflict at least settled into some sort of predictable pattern. The conflict is far from resolved, but it seems to have arrived at what is effectively a stalemate. The US has stopped its bombing campaign, and Iran continues to control the Strait of Hormuz. Investors have accepted this reality and have been high fiving each other nearly every day for a few weeks running. Stocks reclaimed all their lost ground in early April, and have since soared to new record highs.

It’s hard to pin down exactly why risk assets have snapped back with a vengeance even as the clouds on the economic horizon have darkened. Are concerns about higher inflation and slower economic growth – both of which are most certainly ahead – being superseded by a solid start to the 1Q26 earnings season and euphoria over the war not being worse than expected? I suspect these are the major reasons, plus toss in a dose of emboldened retail confidence to buy each and every dip opportunity (which drags institutional investors along), and voila – you achieve record highs in US stocks in no time flat. This is exactly where we are at the moment. Investors who are scratching their heads at this bounce have to recognise that investor psychology and FOMO play a much larger roll these days than fundamentals. And we cannot forget the profound effects that the rapidly growing use of A.I. will have on future productivity, even though the value, magnitude and timing of productivity enhancements are impossible to predict.

What is my response in my portfolio given the one-way march higher?

I made some modest adjustments to my portfolio last week, taking some money off the table on a few names (in small size), including BRB.B and JNJ. I have also written covered calls on a few tech names (AMZN, GOOG) ahead of Mag 7 earnings this week, as I don’t mind losing a few shares of these companies at their new lofty levels. Normally, I would not write covered calls on shares in front of earnings, but the snapback has been very fast and I suspect – earnings aside – that we will see some consolidation in the weeks ahead.

DoJ drops criminal probe into Fed chairman Powell

I count myself as a fierce defender of the Fed’s independence. It has been apparent since President Trump was re-elected that he would go after Fed chairman Powell for not “kissing his ring” and complying with the president’s economically ridiculous request to slash the policy interest rate. The DoJ had nothing on Powell or the Fed from the onset, so – certainly with the administration’s reluctant endorsement – the DoJ dropped its frivolous investigation to clear the way for the Congressional approval of incoming Fed chairman Kevin Warsh. Investors breathed a sigh of relief. Interest rates at the short end of the curve dropped 5bps on the news since Mr Warsh is expected to be more dovish than Mr Powell, although keep in mind that Mr Powell is likely to remain a voting member of the 12-member FOMC.

UK news: some good news, some bad

Early in the week, we got solid UK employment data for March (here), which built on better-than-expected GDP data released April 16 (here). Retail sales figures for March (here) also showed solid growth in war-affected March, even when removing the sharp increase in prices of fuel at the pump. The CPI report for March released midweek (here) was a reminder that inflationary pressures remain problematic, injecting a dose of reality into the precarious position of the U.K. economy. In line with expectations, headline CPI increased to 3.3%/annum in March, up from 3.0% in February, not surprising given the sharp rise in war-related oil prices. Wage growth slowed sharply, too, according to the inflation report. Preliminary PMI data for April was better than expected for both goods and services, in contrast to PMI data in the Eurozone, which was worse than expected. The decent economic data in the U.K. might slightly complicate the Bank Of England’s monetary policy decision this coming week although most investors expect them to sit tight.

On the less good front, an OECD report showed that workers in the U.K. experienced the greatest increase in average tax burden in 2025 of workers in any of the 38 OECD member countries – see right side of graph below from the #FT (article here, subscribers only).

I relied on the FT article rather than combing through the OECD source document, a rather extensive report entitled “Taxing Wages in 2026”. It is clear that a higher tax burden is leading to fiscal drag as far as U.K. economic growth, and this is not helping the U.K retain the portion of its worker base that can move to more tax-friendlier jurisdictions. This is just one more reason that the Labour government remains under intense pressure as they try to thread a needle.

US economic data: still solid for the most part

March US retail sales – which were measured during the “war period – came in better than expected based on the Census Bureau’s advance monthly sales release (here). This illustrates that even though the Trump Administration has adopted some questionable economic policies, the U.S. economy continues to power forward. It is increasingly evident that the size and diversity of the U.S. economy makes the momentum hard to stop, no matter how poor some of the economic policies have been. Like it or not, it’s hard to bet against American exceptionalism, a topic I wrote about last June (here). Having said that, it is equally clear that the wealth gap is widening, and this is what will likely undo the Republican party majority in Congress in the midterms. Should this occur, it will be viewed as a “revolt” by middle class Americans, who are clearly suffering from an affordability crisis (see my article on the K-shaped economy here). The Michigan Consumer Confidence survey released Friday (here) recorded the lowest readings ever, adding further pressure on the Republicans.

What’s ahead?

Economic data releases are light this coming week, as the week will be dominated by four of the major central banks rendering monetary policy decisions (all expected to hold). It is also a big week for earnings, with five of the Mag 7 companies reporting.

Central bank meetings:

Bank of Japan: April 27-28 (likely to hold even though inflation data unfavourable)

FOMC (Fed): April 28-29 (expected hold)

ECB: April 29-30 (expected hold)

Bank of England: April 30 (expected hold)

Earnings of interest, week of April 27: All eyes will be on five of the Mag 7 companies that are reporting this week: MSFT, AAPL, AMZN, GOOG and META are all week of April 27th.

Economic data worth watching:

· US: PCE report for March

· Eurozone: preliminary CPI data (April), 1Q2026 GDP

MARKET DATA AND TABLES

Below are tables of key indices and asset prices that have been updated for the past week.

_________________

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments