Week ended August 22, 2025: Powell signals dovish tilt

- tim@emorningcoffee.com

- Aug 23, 2025

- 3 min read

Risk markets moved sideways to lower most of this past week, until comments by Fed Chairman Powell at the Jackson Hole Economic Policy Symposium on Friday were interpreted as decisively dovish by investors, pushing stocks sharply higher and bond yields lower. You can watch Mr Powell’s comments here (on YouTube) from the symposium website (21 minutes), or read the transcript of his comments here (from Fed website).

Naturally, as an investor that is long risk, a run like the one on Friday is welcomed. However, I was shocked at the magnitude of the gap up because the probability of a 25bps reduction in the Fed Funds rate, according to the CME FedWatch Tool, is 75%, which – in spite of Mr Powell’s comments – is significantly below the probability of only two to three weeks ago, when the probability was 95%. I consider Friday’s sharp rally mainly a relief reaction because the Fed Chairman acknowledged a tilt away from inflation concerns (even though inflation remains elevated), and towards pre-empting a slowing U.S. economy and a weakening jobs market. By moving towards easing, this might get President Trump off Mr Powell’s back. That would be nice in that the president’s ongoing threats around the independence of the Federal Reserve is third-world country stuff.

Although surprised at the magnitude, I do not think the rally has legs because U.S. stock valuations remain at the very high end of what seems reasonable based on historic norms, and the U.S. economy seems to be weakening. In addition, inflation remains above the Fed’s target, and this combination reeks of an economy potentially at risk of a bout of minor stagflation. Not only are stock prices too high in my opinion, but credit spreads in the corporate bond market are too tight, certainly in the context of a potentially slowing U.S. economy. As most, I expect a reduction in the Fed Funds rate will occur at the next FOMC meeting, but unless the jobs market falls off a cliff, I think it will be a hawkish cut in that the Fed will likely say that further reductions will remain data-dependent.

This is the perfect environment for writing covered calls partially on stocks that look nose-bleed high. And it has also coaxed me into restoring some downside protection via out-of-the-money S&P 500 puts (SPY puts) between the end of September and end of December. For the former strategy, it is a way to generate incremental income, and for the latter, it is a matter of paying for insurance given I am very long equities and prefer not to sell shares (hence, preserving potential further upside).

This week, we have the last of the Mag 7 companies reporting earnings (NVDA Wednesday after close), and we will also get rather dated PCE data (Fed’s focus as an inflation gauge) for July on Friday before the U.S. markets open. The next FOMC meeting will be September 16-17, with a monetary decision announced on the second day followed by the usual press comments / Q&A with Chairman Powell. A revised Summary of Economy Projections will also be released then, always an important insight into the Fed’s thinking.

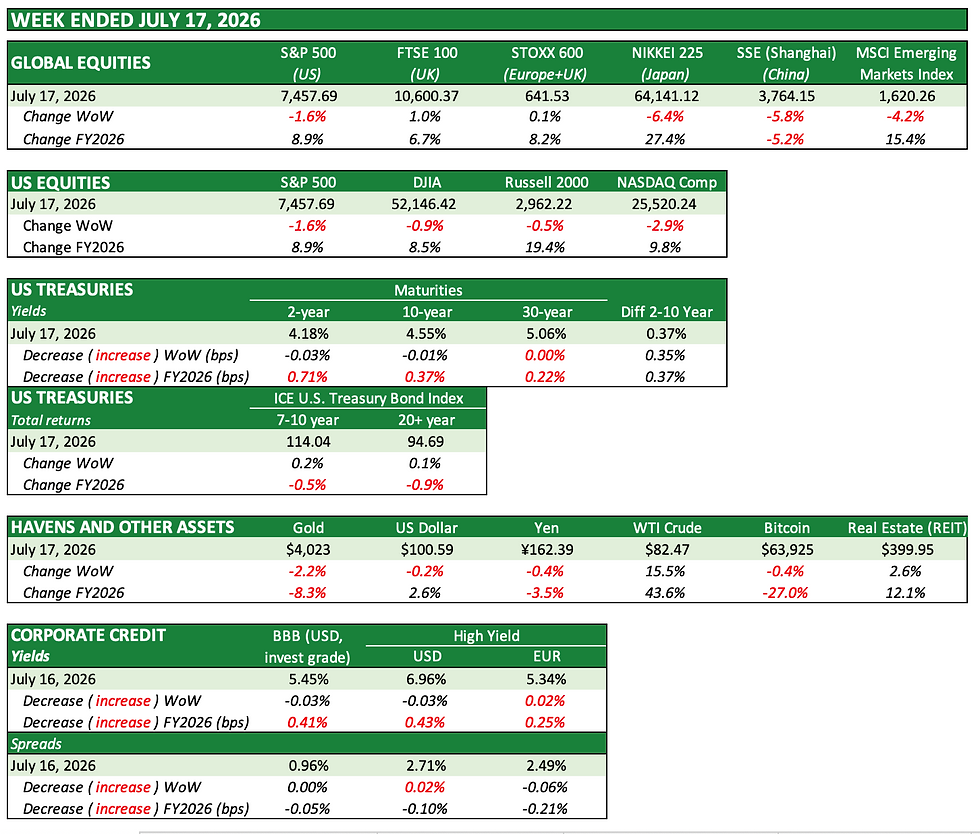

Market summary / tables

As mentioned above, U.S. stocks rallied sharply on Friday, wiping out most of the losses that occurred in the first four trading sessions of the week. Stocks that might benefit most from rate reductions – large cap cyclical stocks and small cap stocks – rallied the most, with the DJIA (+1.5% WoW) and the Russell 2000 (+3.3% WoW) leading gains as far as U.S. stock indices. Globally, Chinese equities were the best performing stocks last week, with European stocks also posting solid gains.

US Treasuries, which were range-bound most of the week, rallied strongly on Friday, too, off the back of a “pencilled in” Fed Funds rate cut in September. For the week, the 2-year and 10-year US Treasuries ended 7bps lower, with total return bond investors realising positive WoW gains. Through Thursday (since there is a delay in data), corporate bond spreads nudged wider, not surprising given the recent run. As I mentioned already, corporate bond spreads remain historically tight, meaning there is more asymmetric risk to the downside from here.

In currencies, the greenback got hammered on Friday as bond yields declined. Gold rallied hard on Friday, somewhat surprising in that arguable risk sentiment improved, but perhaps this was more related to the weakening US Dollar.

_________________

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments