Week ended Feb 13th 2026: US stocks remain under pressure

- tim@emorningcoffee.com

- Feb 14

- 6 min read

I am going to start the update this week by focusing on markets, which is probably what most of my readers care most about. The table below is a summary of the week.

As far as equities, portfolio allocations so far this year have favoured value stocks over growth stocks in the U.S., and international stocks over US stocks on a macro global basis.

U.S. stock rotation: out of growth and into value: As far as U.S. stocks, the culprit continues to be tech shares. As the “long anything/everything A.I. trade” has come under increased scrutiny, tech shares across the board have come off the boil, dragging down those stock indices most concentrated in tech names (like the NASDAQ). Investors have been rotating out of A.I. narrative growth stocks, and reallocating into stocks that are cheaper from a valuation perspective (i.e. “value stocks”). The beneficiaries of this rotation have mainly been small and mid-cap stocks, but also larger and more defensive stocks of companies that are operating in sectors like healthcare, utilities and industrials. The graph below depicts the four indices that EMC tracks, and you can see the relative performance of each index since the beginning of the year. The value-focused Russell 2000 leads gains in U.S. stocks indices in 2026, up 6.6% YtD, while the tech-heavy NASDAQ Comp leads the losses, down 3.0% YtD.

Global stock allocation: out of U.S. stocks and into international stocks: If we focus on the most-followed U.S. stock index – the S&P 500 – the performance has been poor this year vis-à-vis most other international stock markets. You can see this in the summary table at the beginning of this update. European, Asian and broader emerging markets indices have all significantly outperformed U.S. stocks this year. This is in line with the global geographic diversification theme that many pundits (including this one) have been recommending for several months running. Teh graph below illustrates the performance of the S&P 500 (black line) YtD, compared to two emerging markets regions (Asia Pacific and Latin America) and the all-world index ex-USA.

In essence, favouring equity markets outside of the U.S. is a backhanded “value” play, since U.S. stocks remain expensive vis-à-vis many other global markets. However, be aware that the gap is closing. If you are a non-U.S. investor that is investing in U.S. stocks, the erosion of value in the greenback has made a bad situation worse. The U.S. Dollar remains under severe pressure, already down 1.2% YtD against the DX-Y (following a sharp decline in 2025).

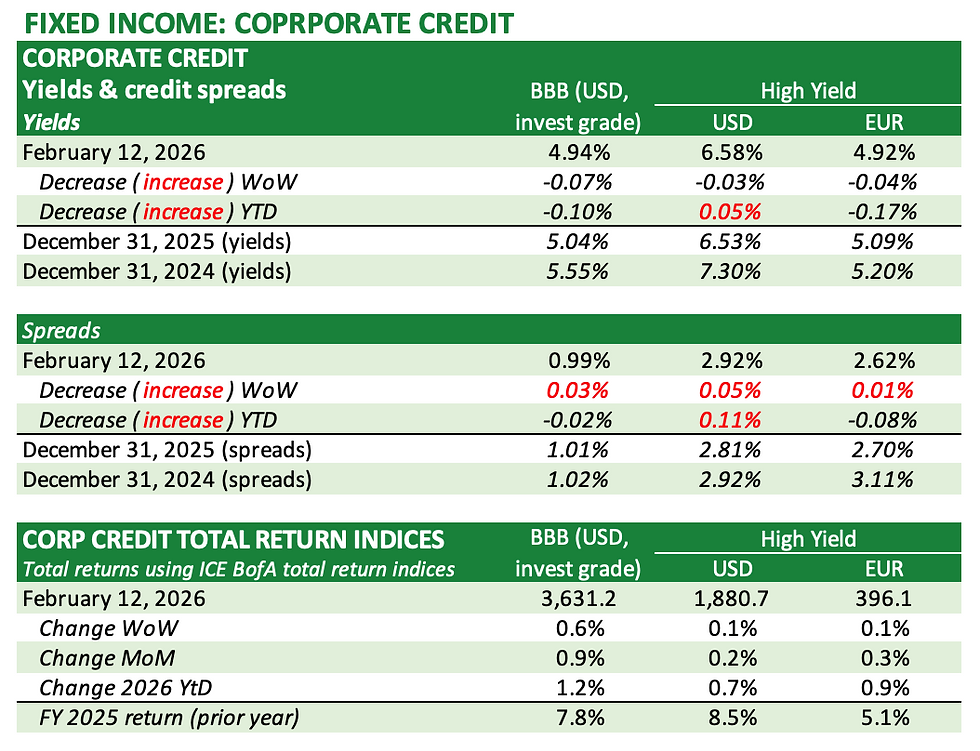

As far as fixed income (aka bonds), U.S. Treasury bonds bounced around the first half of the week, with each move corresponding to the latest economic data release. However, the last two trading sessions of the week were very positive for long-duration holders of bonds. A flight-to-quality on Thursday pushed Treasuries higher as U.S. equities unravelled, followed by a tame January CPI report released Friday morning which gave bonds a another shot in the arm. Yield tightening was most severe at the intermediate and long end of the curve. The yield on the 10-year Treasury looks to have finally pierced a resistance point as it heads back towards the magical 4% threshold. Corporate bonds responded accordingly from a yield perspective, although the combination of huge primary (new) bond issuance (see GOOG bond discussed below) and a wobbly stock market has not been as kind to credit spreads.

In other asset classes, gold has surged back above $5,000/ounce, even as cryptocurrencies remain under severe pressure. BTC has by far been the poorest performing asset class tracked by EMC this year. In currencies, the greenback lost ground as the Yen strengthened. Concerns about Iran/Middle East tensions have faded a bit, as oil prices fell, continuing to trade in a range that I consider slightly to the stimulative side of neutral.

More detailed updated tables can be found in the weekly update on the website / at the bottom of this update.

WHAT MATTERS NEXT WEEK

U.S. stock and bond markets are closed on Monday for a U.S. holiday.

Economic data: 4Q25 GDP growth for Japan will be released on Monday; U.K. CPI for January and minutes from the last FOMC meeting on Wednesday; and a slew of PMI manufacturing, services and composite data for the U.S., the U.K. and the Eurozone on Friday.

Earnings: 78% of S&P 500 companies have reported earnings. “This Week in Earnings” (#LSEG I/B/E/S) states that expected YoY growth (4Q25 vs 4Q24) for revenues and earnings for S&P 500 companies is expected to be +8.6% and +13.6%, respectively. 53 more companies report earnings this coming week, of which the most watched is likely to be Walmart (W) before the open on Thursday (Feb 19th). NVDA will be the last of the Mag 7 companies to report on Feb 25th.

The U.S. government is heading towards another partial shutdown on Saturday. It feels like it’s just another day at the office.

NEWS THAT MATTERED LAST WEEK

US economic data

We got a slew of economic data for January this past week, perhaps none more important than the January jobs report and January CPI, both delayed due to the government shutdown in the autumn.

The US jobs report surprised on the upside for January, with payroll additions (130,000) exceeding expectations, and the unemployment rate remaining steady at 4.3%. As surprisingly good as this was to start the year, new jobs added for 2025 were revised down to 181,000 for the entire year, the lowest outside of recession periods since 2003.

The January jobs report was a reminder of the resiliency of the U.S. economy and an important marker for investors.

CPI data, released Friday before the open, also came in better than expected with headline and core CPI for January falling to 2.4% and 2.5% (YoY), respectively. The bond market liked the CPI figures and rallied accordingly. The CME FedWatch Tool continues to forecast two 25bps reductions in the Fed Funds rate in 2026, although the odds look around even for a potential third reduction at the end of the year.

Alphabet raises $32 billion equivalent in multi-tranche bond issue

To address its seemingly insatiable need for capital to finance the rollout of A.I., tech giant GOOG raised nearly $32 billion equivalent in a multi-tranche bond issue early last week. I’m a former bond bro’, so the amount raised, as well as the combination of tenors and currencies, is truly impressive. In addition to issuing $20 billion of bonds in a seven-part US Dollar denominated issue (longest tenor 40 years), GOOG issued the largest-ever series of corporate bonds in Sterling (£5.5 billion) and Swiss Francs (CHF 3.055 billion). The five-part Sterling issue also included an unusual “century bond” (100 year maturity), with £1 billion issued at this unusually long tenor (at a price of 120bps over Gilts). The success of the GOOG bond issue illustrates the ongoing appetite of global fixed income investors who seem more than happy to lap up the debt of highly-rated hyperscalers in order to help them finance their gigantic A.I.-related capex programmes.

Japanese election

Japanese stocks – the best performing stock index tracked by EMC – jumped to record levels last week after Prime Minister Sanae Takaichi’s landslide win in a snap general election on Sunday. The Nikkei 225 benchmark rose as much as 5.7 per cent on Monday, breaking through the 57,000 level for the first time. Investors view PM Takaichi as a leader that will look to stoke the fiscal pump, priming the Japanese economy for better growth even as inflation remains elevated. Does that narrative sound familiar?

E.U. remains complicated and “confused”

France’s president Emmanual Macron said this past week that the E.U. needs to press forward with “making more goods in Europe” in order to help its economy, and reduce its dependency on U.S. (less reliable) and Chinese goods. According to Mr Macron, this strategy entails making more things in Europe, even if the costs are not competitive globally. I cannot disagree with Mr Macron as far as his broader objective, but his solution would undoubtedly prove counter-productive in the long run. I thought Swedish prime minister Ulf Kristersson provided a more honest assessment of what the E.U. should not do, stating in an #FT article (here):

“The basic idea of trying to protect European business, if that is the purpose of Buy European, to try to avoid trading with or partner with other countries, then I’m very sceptical,” Kristersson told the FT in an interview. “We need to be able to compete because of quality and because of innovation, not because we try to protect the European markets.”

MARKET DATA AND TABLES

_________________

**** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. ****

Comments