China Evergrande Group: What now?

- tim@emorningcoffee.com

- Sep 20, 2021

- 7 min read

All eyes are currently focused on China Evergrande Group (“Evergrande”), the largest (or second largest, depending on source) property developer in China. A proper and in-depth analysis of the situation regarding the company’s debt would take extensive time, so let me instead distil this down to the principal issues and why investors are concerned.

1. Debt / liabilities profile and liquidity

2. Credit ratings history

3. Potential “losers” in an Evergrande default

4. Contagion risks

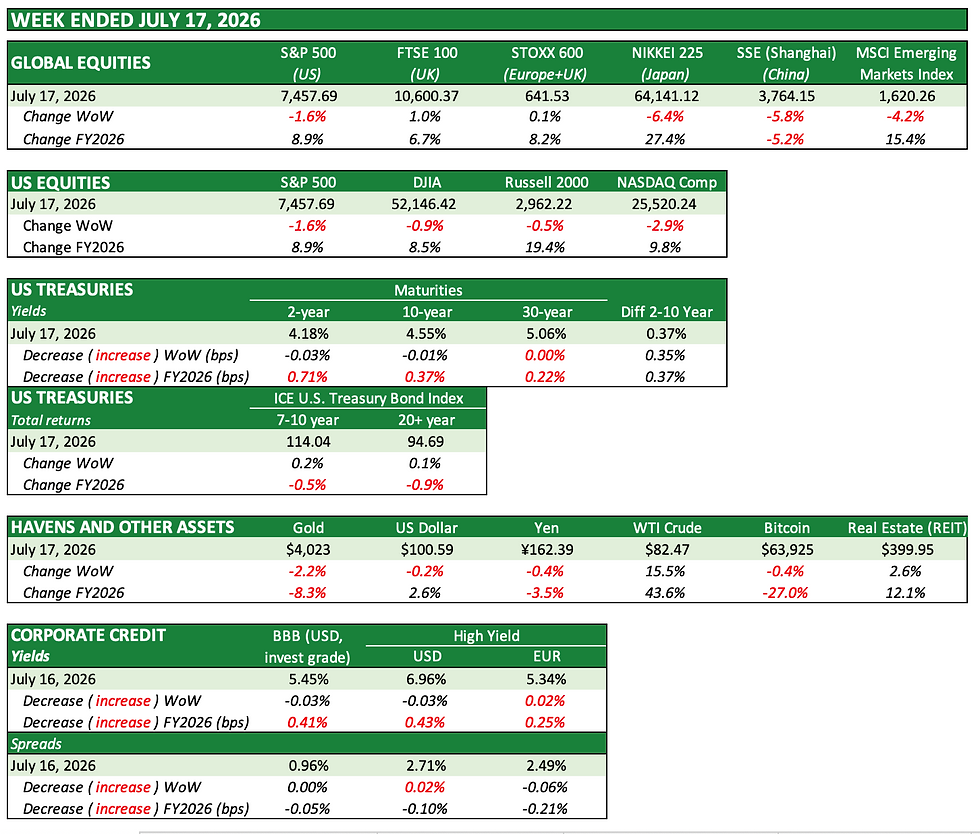

Using the share performance as a proxy of Evergrande’s ongoing viability, concerns began to surface in late first quarter / early second quarter, but accelerated in the early summer as you can see in the graph below.

1. Debt/ liabilities profile and liquidity

Evergrande’s latest interim financial statements for the six months ended June 30th 2021 are here. The financials are presented in RMB, and for purposes of converting to USD, there are about RMB 6.5 / USD 1.0. As far as core business, Evergrande employs 200,000 people and owns more than 1,300 projects in more than 280 cities in China. About 90% of the company’s RMB 226.7 bln of revenues for the six months ended June 30th 2021 was from property development, the core business of Evergrande. According to Statista, Evergrande is the largest Chinese property developer by revenues (RMB 507 bln in 2020), followed by Country Garden (RMB 463 bln), Greenland Holdings (456 bln) and Vanke (RMB 419 bln).

Evergrande had total debt of RMB 571.8 bln at June 30th 2021, with unrestricted cash on hand of RMB 86.8 bln. Of the RMB 571.8 bln of debt, RMB 240 bln is due this year, and another 156.8 bln is due between 1-2 years. In addition to its large amount of debt, the company has RMB 215.8 bln of contract liabilities due (which I believe means properties contracted but not completed and closed), against restricted cash (deposits I presume) of RMB 74.9 bln. Any way you look at it, the company has financed itself using predominantly shorter term debt and customer deposits, which makes it highly dependent on continued access to the debt markets (bank and bond markets) and to advances on property sales simply to address maturing debt. The company has been trying to sell non-core assets for more than two years to reduce debt, at the same time heavily promoting new property sales because deposits are obviously an important component of the company’s liquidity.

Most of the company’s debt is denominated in RMB so is from “on-shore” creditors. As of June 30th 2021, 23.7% of Evergrande’s debt was denominated in USD or HKD (linked to USD). I could not find a more granular breakdown of creditor groups, but broadly, the lender groups comprise i) Chinese banks, ii) Chinese bond investors, and iii) foreign bond investors. I am not sure how exposed non-Chinese banks are to Evergrande or to the Chinese property market more broadly, but I do assume that credit has been provided by foreign banks, too.

2. Credit ratings history

Evergrande us a classic non-investment grade rated company, recognising its sector (property development), its jurisdiction (China, an emerging market) and its aggressive use of leverage. The company is now rated Ca by Moody’s, CCC by S&P, and CC by Fitch, with all three rating agencies having downgraded Evergrande in the last few weeks. The company’s foreign-denominated bond issues are rated one or two notches below the family ratings (C/CCC-/C), all of which signal an imminent default. According to various press articles, Evergrande’s foreign debt is trading around 25 cents on the dollar, at severe distressed levels. Prior to the acceleration in concerns about liquidity, all three rating agencies had Evergrande rated strong/mid B.

3. Potential “losers” in an Evergrande default

Losers in a default by Evergrande would include customers, employees, suppliers and creditors. Of these categories, I would expect the most important – certainly from the standpoint of the Chinese government – would be customers that have put down deposits on new properties which have not been completed and delivered. As I mentioned above, Evergrande seem to be holding around RMB 75 billion in customer deposits for uncompleted projects and needs RMB 216 billion to complete these projects. Without access to additional liquidity, the completion and delivery of these projects will be in jeopardy. I suspect as the Chinese government is considering whether or not Evergrande is “too big to fail”, its first priority will be to protect customers. The press has reported that there have been customer protests throughout China recently regarding Evergrande’s precarious financial position, so customers will be a key area on which to focus. With over 200,000 employees, Evergrande is also a significant employer in China, and the repercussions of the winddown of such a significant employer would be far-reaching. Suppliers would also be affected if Evergrande were to be wound down. Evergrande owes plenty of money to suppliers: trade payables at June 30th 2021 were RMB 667 bln, of which around 87% is due in one year. In fact, the amount of trade credit is larger than the company’s debt! I can only speculate as to the type of suppliers, but they would include any company that provides materials or service work for the completion of a house or commercial property – wood / timber companies, steel companies, paint companies, concrete companies, and so on, plus what must be tens of thousands of small subcontractors.

This brings us to the last category of affected parties, which is also the one grabbing the headlines – creditors. As far as creditors, it is a two-tier system. Because the largest Chinese banks are state-owned, I would expect any sort of lifeline from domestic banks to Evergrande would be government “supported”. Rolling maturing loans would buy the company time to ensure, for example, that properties are completed so that customers who have paid deposits are not harmed. Without government prodding, no creditors would likely continue to lend to Evergrande given the precarious state of the company as far as liquidity at the moment. However, the real focal point will be when the next payment on foreign debt is due since the government cannot easily influence the actions of foreign creditors. I have doubts that the government would want on-shore money to leave the country to bailout foreign creditors. In addition, it would be a clear issue of morale hazard, and future lenders might become “comfortable” making risky loans to systemically important Chinese companies on the basis that they would be rescued if things went wrong. This leads me to my conclusion that Evergrande will attempt to undertake a voluntary restructuring so that the company can continue to operate albeit on a scaled-down, less leveraged and more focused basis. Even in this scenario, I would certainly be much more nervous as a foreign creditor than a domestic on-shore lender or bondholder.

4. Contagion

Contagion is the principal risk at the moment. Should the company default, the risk would not be entirely contained, but would be most severe in China since Evergrande is principally a domestic business. Chinese banks are the largest creditors. Although I suspect that Chinese banks can withstand the default of an individual borrower, even one the size of Evergrande, the more severe risk is that lenders pull back from lending to the Chinese property sector more broadly, an important driver of the Chinese economy. Foreign lenders and investors would also be negatively affected and would take severe losses on written-down positions (if not already written down).

Based on a cursory review, it seems the larger benchmark indices and ETFs focused on US and European high yield are not involved in Evergrande bonds, which are instead the focus of Asian high yield funds and perhaps global hedge funds. I would expect distressed debt investors to get increasingly involved in the Evergrande bonds as things progress because these bonds are an obvious play in an environment where there are few distressed debt opportunities given the frothy state of markets. It is this specialty-category of investors which I suspect would be around the table to drive an orderly restructuring or pre-packaged bankruptcy of the company. It would be in everyone’s interest to go down this path, and to avoid the extensive disruption of disorderly near-term bankruptcy filing without a clear exit plan.

Given that Evergrande is a Chinese company, I would not expect contagion into US or European high yield funds or indices (since they do not buy emerging markets high yield bonds). The access to on-shore and off-shore capital of Chinese property companies more broadly will be negatively affected, at least temporarily, as I suspect customers, creditors and suppliers will be looking much more closely at the financial strength of Chinese property companies with which they do business. Having said all this, it is really the government that is in a bind. It can let Evergrande fail and face the consequences not only of Evergrande, but of the Chinese property market more broadly, which would then put the economic growth of China at risk. Or it can provide a lifeline (or encourage local state-owned banks to do so), a type of morale hazard which might encourage creditors – both on-shore and off-shore – to continue to lend aggressively to Chinese companies on the basis that the government will save systemically important companies in the future, should they run into trouble.

Conclusion

I suspect Evergrande will be restructured, and that the Chinese government will not allow the company to fail completely. The trigger point is likely to be when the company faces a payment on foreign debt, which I understand is in the coming days or weeks. Without a viable plan of restructuring, foreign creditors will demand repayment of their debt, and the company will default because it clearly does not have access to capital to meet its heavy immediate redemptions and payments to suppliers. The Chinese government will play along but will be conscious of morale hazard, likely choosing not to bail out foreign creditors at 100 cents on the dollar. Rather, I expect foreign creditors – with the participation of Chinese (state-owned) banks – to take the requisite haircuts to allow the company to carry on operating so that Chinese customers are not harmed, and suppliers remain engaged. The collateral effects of an Evergrande restructuring on other financial markets, like US high yield or property developers in other countries, should not be material because the attributes of the Chinese property market and the company’s significant reliance on short-term debt are hopefully rather unique.

** Follow E-MorningCoffee on Twitter, and please like and comment on my posts right here on my blog. You need to be a subscriber, so please sign up. Thanks for your support. **

Awesome article, thanks Tim. I was just discussing with my friends this morning and we only had a very preliminary understand as to what was going on. I’ve passed this along to all of them.

I’m most curious about the contagion here. It looks like US markets are reacting despite the fact that they apparently have little direct skin in this game.

I really don’t see the Chinese government letting the company go under, it would be too disastrous for too many reasons.

Thanks again!

Charles

Nice piece Tim and I agree with your conclusions. This is one of the occasions where 'state controlled capitalism' will appear (at least in the short term) to have benefits, and no doubt they will 'calm' markets down once the govt is ready and dish out the requisite haircuts. 2008 was very different to this scenario.